“I can afford to purchase a home?!”

This is something I often hear from clients when I explain that they don’t always need 20% down payment to purchase. Many buyers have the misconception that a large down payment is required, which stops them from considering a purchase or leaves them stuck in a lower price range. And I am not the only agent dealing with this myth.

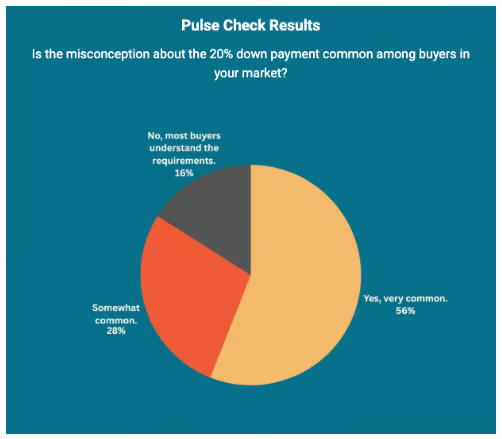

According to a survey conducted for The Close’s newsletter, a majority of real estate agent respondents (56%) indicated that the 20% down payment misconception remains very common among buyers in their markets, and 28% identified it as somewhat common. This survey reinforces the need for buyer education to be a top priority for agents to capture buyers stuck on the sidelines.

How’d the misconception start?

There are benefits to putting 20% down, but many buyers believe it’s the only way to purchase a home. And that is just entirely false. The misconception stems from historical lending standards, when putting 20% down was once considered the traditional requirement for mortgage approval and protection against lender risk.

Over time, the idea continued to spread through generations, financial advice, and outdated homebuying assumptions, leading many buyers to believe they need a massive amount of savings just to enter the market. For many potential homeowners, that belief alone has delayed the buying process before they ever explored what loan options were actually available.

What’s the reality?

Unless your client’s lender states otherwise, 20% down is not required. There are a variety of loan options and a multitude of factors that determine a buyer’s required down payment. For example, FHA loans require as low as 3.5% down, while a conventional loan’s minimum is typically 3% to 5%. There are even options, such as VA and USDA loans, that allow qualified applicants to purchase with zero percent down.

Now you may be wondering what buyers are actually putting down? According to the National Association of Realtors, the median down payment for first-time buyers is only 10%. This data further reinforces how outdated the 20% myth truly is, and once enlightened, buyers are taking advantage of lower down payment options.

What this misconception is actually doing to buyers

One of the biggest issues with the 20% down payment myth is that it leads many buyers to believe they are much further from homeownership than they actually are. Instead of exploring their financing options early, many buyers spend years trying to save an unrealistic amount of money before ever speaking to a lender.

In many cases, this misconception also causes buyers to limit themselves financially before they even begin the home search. Some buyers remain stuck in lower price ranges or continue renting because they assume a large home automatically requires a massive upfront payment.

Once buyers better understand today’s loan options and down payment requirements, many realize they may be in a stronger position to purchase than they originally thought.

Agent playbook

Agents, you’re probably wondering how to help buyers overcome this misconception. Thankfully, there are plenty of ways to educate buyers and make the process feel more accessible.

- Social media videos: Create short-form videos explaining common down payment myths, loan options, and real-world examples buyers can relate to. I’ve personally created videos on this topic and have seen great engagement and conversations come from educating buyers this way.

- Print marketing: Use flyers, mailers, or handouts with simple financing facts and down payment statistics to educate your local audience.

- Mortgage lender partnerships: Partnering with trusted mortgage lenders can help buyers better understand their financing options early in the process. When in doubt, always encourage buyers to speak directly with a lender so they are fully aware of all loan programs and down payment options available to them.

- Buyer consultations: Include down payment myths, financing education, and loan examples to help clients feel more informed and confident throughout the process.

- Buyer events: Hosting first-time homebuyer events is a great way to walk buyers through the homebuying process in a low-pressure environment. I’ve personally hosted these events and found them to be extremely valuable for educating buyers and building trust. Consider inviting mortgage lenders, attorneys, inspectors, and other real estate professionals to answer questions, and don’t underestimate the value of providing food and drinks to create a welcoming atmosphere.

Takeaway

The 20% down payment myth highlights a much bigger reality in today’s housing market: many buyers are not being held back by their finances alone, but by outdated assumptions about what homeownership actually requires. To successfully guide clients through a transaction, agents need to understand not only their goals but also the fears, misconceptions, and hesitations that shape their decisions.

One of the biggest lessons I learned throughout my real estate career was the importance of asking the right questions, understanding a buyer’s mindset, and identifying what may be holding them back before jumping straight into the home search. Many buyers simply don’t realize that loan programs and financing options are available that make homeownership far more attainable than they assumed.

As the market continues to shift, buyer education is becoming one of the most valuable tools agents have for building trust and generating future business. Agents who proactively educate buyers through conversations, social media, marketing campaigns, and buyer events are positioning themselves as trusted advisors rather than just salespeople.

In a market where information is everywhere but clarity is rare, the agents who help buyers move past misconceptions and confidently understand their options will be the ones who stand out and build long-term relationships.

Check out some of our newsletters: