Buying a home is a major milestone that is both exciting and complex. From preparing finances to closing-day logistics, there are dozens of moving parts that can overwhelm even the most confident buyers. This comprehensive guide to home buying breaks the process into clear, manageable steps, helping buyers stay organized, avoid costly mistakes, and move smoothly through each phase of the transaction.

A home buyer’s checklist acts as a roadmap and helps buyers stay informed every step of the way. For agents, it’s a powerful tool that sets expectations early and reduces friction later. Instead of reacting to deadlines and surprises, buyers can move proactively through the process with clarity.

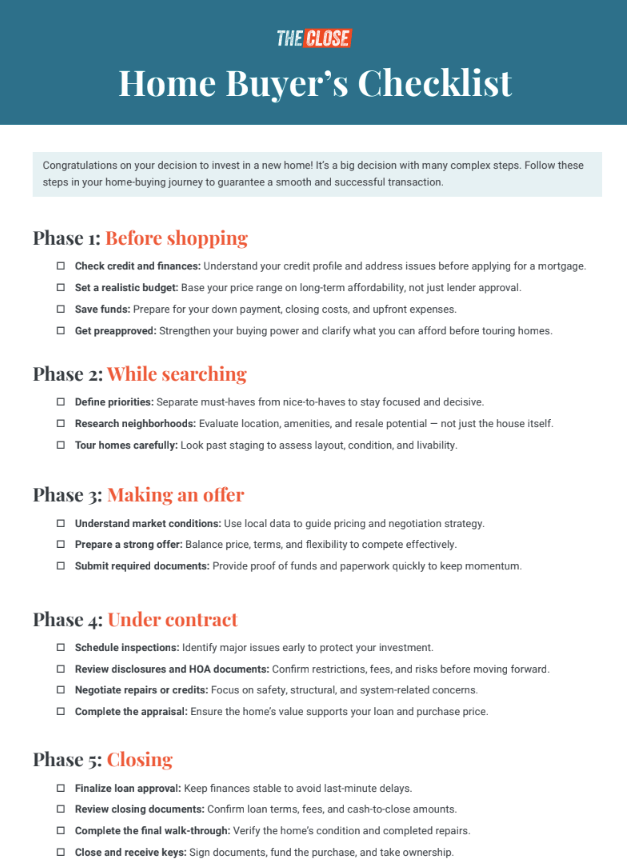

Download our PDF home buyer’s checklist below:

- Phase 1: Financial preparation (before house hunting)

- 2. Set a realistic budget

- 3. Save for upfront costs

- 4. Get preapproved for a mortgage

- Phase 2: Home search checklist (finding the right property)

- 5. Define must-haves vs nice-to-haves

- 6. Research neighborhoods

- 7. Tour homes strategically

- Phase 3: Making an offer

- 8. Understand local market conditions

- Phase 4: Under contract

- Phase 5: Final loan and closing

- Home buying do’s and don’ts

- Your take

Phase 1: Financial preparation (before house hunting)

1. Review credit and financial health

Before looking at homes, buyers should understand their financial standing. Checking credit early gives buyers time to correct errors, improve scores, and qualify for better loan terms. Even small changes, such as paying down balances or correcting reporting errors, can have a meaningful impact on interest rates and monthly payments. Strong financial health also makes the overall buying process smoother and less stressful.

Checklist items:

- Check credit scores from all three bureaus (Equifax, Experian, and TransUnion)

- Dispute errors or inaccuracies

- Avoid opening new credit accounts

- Pay down high-interest debt

2. Set a realistic budget

A realistic budget considers not just what a lender approves, but also what buyers can comfortably afford over the long term. Factoring in lifestyle goals, future expenses, and savings priorities helps prevent becoming house-poor. Buyers who set clear financial boundaries are more confident and decisive during the search.

Buyers should account for:

- Monthly mortgage payment

- Property taxes and insurance

- HOA fees

- Maintenance and repairs

- Utilities and commuting costs

📌 Pro Tip

Work with your buyers to establish a realistic budget based on their income, expenses, and savings. Share this mortgage calculator, which they can use to understand how much home they can afford.

3. Save for upfront costs

Beyond the down payment, buyers need cash reserves for several upfront expenses. Many buyers underestimate how much cash is needed before move-in day. Closing costs, deposits, and moving expenses can add up quickly, especially in competitive markets. Building reserves early reduces last-minute financial stress and protects buyers from unexpected costs.

Beyond the down payment, buyers need cash reserves for:

- Earnest money deposit

- Closing costs, which include lender fees, third-party services, government services, and other prepaid items (typically 2% to 5% of purchase price)

- Moving expenses

- Initial repairs or furnishings

4. Get preapproved for a mortgage

Mortgage preapproval is essential in competitive markets. A preapproval shows sellers that a buyer is serious, qualified, and ready to close. It also gives buyers a clear understanding of their price range before emotions get involved. Comparing lenders at this stage can result in better rates, lower fees, and smoother underwriting later.

Buyers should:

- Compare multiple lenders

- Understand loan options

- Lock in rates strategically

- Review estimated monthly payments

Phase 2: Home search checklist (finding the right property)

5. Define must-haves vs nice-to-haves

Clear priorities prevent decision fatigue during the home search. When buyers know what they truly need versus what they’d simply like, it’s easier to evaluate homes objectively. This clarity also helps agents narrow options and avoid wasted showings. Priorities may evolve, but having a baseline keeps expectations realistic.

Common must-haves include:

- Location or school district

- Number of bedrooms/bathrooms

- Commute time

- Outdoor space

6. Research neighborhoods

Neighborhood research helps buyers understand long-term livability and resale potential. Factors like amenities, development plans, and overall feel of the community can dramatically affect satisfaction after move-in. Encouraging buyers to explore areas beyond listing photos leads to better decisions.

Buyers should evaluate:

- Local amenities and walkability

- Crime rates

- School ratings

- Future development plans

- Resale potential

7. Tour homes strategically

When touring properties, buyers should look beyond staging. Open houses and showings are opportunities to evaluate how a home actually lives day to day. Buyers should pay attention to layout, light, noise, and maintenance — not just finishes. Asking practical questions during tours prevents surprises later.

📌 Pro Tip

Encourage buyers to schedule showings at different times of day (i.e., weekday morning and an evening or weekend). This makes it easier to spot changes in natural light, noise levels, traffic flow, and neighborhood activity, helping buyers avoid surprises after move-in and feel confident about their decision.

Checklist reminders:

- Assess layout and flow

- Check natural light

- Note storage space

- Listen for noise

- Look for signs of deferred maintenance

Related read: Open House Ideas That Will Actually Get You Leads

Phase 3: Making an offer

8. Understand local market conditions

Offer strategy depends heavily on market dynamics. Knowing whether the market favors buyers or sellers shapes pricing, contingencies, and negotiation leverage. Agents play a key role in interpreting data and setting expectations. Buyers who understand market conditions are less likely to overpay — or miss out entirely.

Buyers should know:

- Average days on market

- Sale-to-list price ratios

- Level of competition

- Seller motivations

9. Prepare a competitive offer

A strong offer considers more than just price. Terms, timelines, and flexibility often matter just as much to sellers. Buyers who understand which levers they can pull, without overextending, are more competitive. Strategic offers balance protection with appeal.

Help your buyers determine a fair offer price based on current market conditions, comparable sales, their budget, and the property’s unique features. Encourage competitive bidding based on market conditions in your locale. Lastly, explain the components of a strong offer and how to make their bid stand out.

Key components:

- Purchase price

- Earnest money amount

- Contingencies (e.g, inspection, financing, appraisal)

- Closing timeline

- Seller concessions

📌 Pro Tip

Negotiate the offer on their behalf to secure the best possible terms and price.

10. Submit required documents

Preparation and organization are critical at this stage. Missing or incomplete documents can delay acceptance or weaken an offer. Buyers who respond quickly and accurately signal reliability to sellers and agents. Staying organized here sets the tone for the rest of the transaction.

Buyers should be ready to provide:

- Proof of funds

- Preapproval letter

- Identification

- Disclosures or addenda

Phase 4: Under contract

11. Schedule the home inspection

Home inspections uncover issues that aren’t visible during showings. Attending the inspection helps buyers understand the home’s systems and maintenance needs. Inspection results often guide negotiations and future budgeting.

Buyers should:

- Hire a licensed inspector

- Attend the inspection whenever possible

- Ask questions about maintenance and lifespan

📌 Pro Tip

Provide your clients with a list of reputable home inspectors and explain the importance of a thorough property inspection. Offer to attend the inspection with them and help them interpret the findings.

12. Review disclosures and homeowner association (HOA) documents

This step is often overlooked — but critical. Disclosures and HOA documents reveal restrictions, fees, and risks that affect long-term ownership. Buyers should review these carefully and ask questions early. Surprises discovered late can derail deals or cause buyer’s remorse.

Checklist items:

- Seller disclosures

- HOA rules, fees, and reserves

- Special assessments

- Rental restrictions

13. Negotiate repairs or credits

Inspection findings often lead to renegotiation. Not every issue warrants a request, but major concerns should be addressed. Successful negotiations focus on safety, structural integrity, and system functionality. Clear communication between buyers, agents, and sellers keeps deals moving forward.

After inspection, buyers may:

- Request repairs

- Ask for credits

- Renegotiate price

- Proceed as-is

14. Complete the appraisal

Lenders require appraisals to confirm property value. If an appraisal comes in low, buyers have options — but timelines are tight. Agents often help challenge values or renegotiate terms. Understanding this process prevents panic and rushed decisions.

If issues arise:

- Renegotiate price

- Increase the down payment

- Challenge the appraisal (with comps)

- Exercise appraisal contingency

Phase 5: Final loan and closing

15. Secure final loan approval

Lenders re-verify financial details before closing, so buyers must avoid changes that could raise red flags. Even small financial shifts can delay or derail approval. Staying disciplined ensures a smooth path to closing day.

Buyers should avoid:

- Changing jobs

- Opening new credit accounts

- Making large purchases

16. Review the closing disclosure

The closing disclosure outlines the final loan terms. Buyers should review this document carefully to confirm accuracy. Comparing it to the original loan estimate helps catch discrepancies. Asking questions early prevents last-minute surprises at the closing table.

Review carefully:

- Loan terms

- Interest rate

- Monthly payment

- Cash to close

- Fees and credits

17. Conduct the final walk-through

The final walk-through protects buyers before closing. It’s the final opportunity to address issues before ownership transfers. Schedule a final walk-through of the property with your buyers, ideally a day before or on the day of closing. This is to confirm that the agreed-upon repairs are complete and the home is in the expected condition. Review the closing documents with your clients in advance, explaining each item and answering any questions they may have. Coordinate with the title company, lender, and seller’s agent to ensure a seamless closing experience.

The final walk-through ensures:

- Repairs are completed

- Property condition hasn’t changed

- Appliances and systems function

- Seller’s personal items are removed

18. Close on the home

Closing day finalizes the purchase. Buyers sign documents, transfer funds, and officially become homeowners. Understanding what to bring and expect helps the day go smoothly. Once keys are in hand, the home-buying journey becomes homeownership.

Closing day checklist:

- Bring a valid ID

- Wire funds or bring a certified check

- Sign final documents

- Receive keys and possession details

📌 Pro Tip

Congratulate your buyers on their new home and present them with a thoughtful closing gift to show your appreciation for their trust in your services.Ready to make your move with confidence? Understanding the best and worst times to buy a house heading into 2026 can give you a critical edge in today’s shifting market. Whether you’re planning to buy soon or simply watching trends, knowing how seasonality, interest rates, and local conditions affect timing can help you save money and avoid costly mistakes.

Home buying do’s and don’ts

The home-buying process is full of important decisions, and a few smart moves (or mistakes) can have a lasting impact on your finances and peace of mind. Here are my expert do’s and don’ts tips that you can share with your current and future clients:

Do’s

- Get preapproved early: It clarifies your budget and strengthens your offer in competitive markets.

- Budget beyond the mortgage: Plan for taxes, insurance, maintenance, and HOA fees.

- Research neighborhoods carefully: Location, amenities, and resale potential matter as much as the home itself.

- Attend the home inspection: Seeing issues firsthand helps you understand what’s minor versus major.

- Ask questions throughout the process: Informed buyers make better decisions and avoid surprises.

Don’ts

- Skip financial prep: Shopping before checking credit or savings often leads to disappointment.

- Max out your budget: Just because you’re approved for a price doesn’t mean it’s comfortable long term.

- Waive protections casually: Inspection and appraisal contingencies protect your investment.

- Make major financial changes: New credit, job changes, or big purchases can derail loan approval.

Rush the decision: A smart purchase balances timing, finances, and long-term goals.

Your take

A successful home purchase isn’t about rushing — it’s about preparation. This 2026 complete first-time home buyer’s checklist gives buyers clarity at every stage while helping agents deliver a smoother, more professional experience.

When buyers know what to expect and when to act, they’re empowered to make smarter decisions and, in the process, enjoy the journey to homeownership. Remember, as a real estate agent, you are their trusted partner, so be ready to offer your expertise, answer their questions, and celebrate their successes.