Even the most diligent real estate professionals face legal issues. Whether it’s a missed disclosure, an incorrect property description, or a clerical error, these issues can lead to costly disputes. Real estate errors and omissions (E&O) insurance protects agents and brokers from the financial fallout of errors, oversights, or negligence during property transactions. This coverage is essential to ensure one misstep doesn’t jeopardize one’s career or business. I’ll discuss what errors and omissions insurance in real estate is, what it covers, costs for insurance premiums, and how to file a claim.

- What Is Errors and Omissions in Real Estate?

- What Does Real Estate E&O Insurance Cover?

- Real Estate Errors and Omissions Claims Examples

- Why Do Agents Need E&O Insurance?

- Costs of E&O Insurance for Real Estate

- How to Select an E&O Insurance Provider

- How to File a Claim Through E&O

- Bringing It All Together

What Is Errors and Omissions in Real Estate?

The real estate term errors and omissions insurance is a type of liability insurance for both businesses and individuals. In real estate, E&O insurance will cover mistakes or oversights made by real estate professionals during their work. These mistakes can include failing to disclose important information about a property, providing inaccurate advice, or making clerical errors in contracts. Even with the best intentions, successful real estate agents and brokers can cause errors that lead to financial losses or legal disputes for their clients.

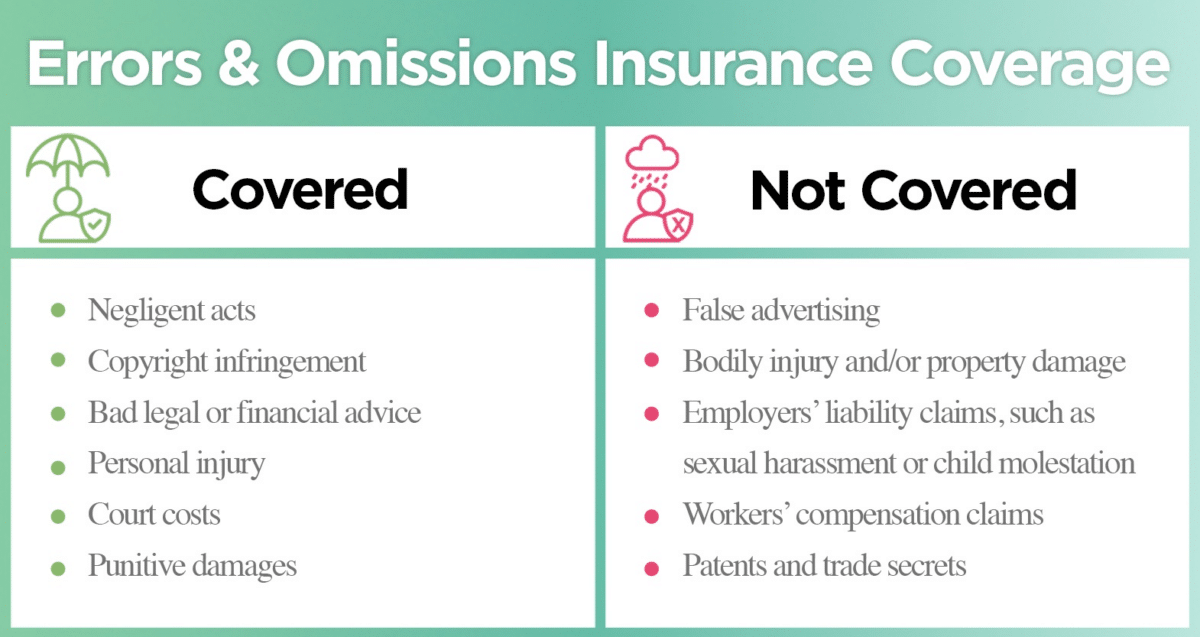

What Does Real Estate E&O Insurance Cover?

Various situations can cause a real estate professional to leverage their insurance, such as misrepresentation, failure to disclose critical property information, negligence, and even accusations of fraud. The insurance typically covers legal defense costs, court fees, and settlements or judgments resulting from such claims, a huge plus for real estate agents.

Real Estate Errors and Omissions Claims Examples

Knowing common examples of an E and O insurance real estate claim is important in avoiding dealing with such claims.

Example 1

Jane is a diligent real estate agent and proudly sells a charming house to a young couple. However, she unknowingly missed disclosing a crucial detail: the roof has a persistent leak. Months later, after a heavy rainstorm, the couple discovers the issue and faces significant repair costs. Feeling deceived, they file a claim against Jane for not providing this essential information. Without E&O insurance, Jane would be on the hook for hefty legal and financial repercussions. This scenario underscores the critical role of E&O insurance in protecting agents from unexpected oversights.

Example 2

John lists a beautiful property and mistakenly advertises it as having four bedrooms instead of three. A family excitedly goes for an open house only to realize the error. Feeling misled, they filed a claim against John for the discrepancy. This everyday mistake quickly escalates into a significant issue, highlighting the necessity of E&O insurance for real estate professionals. E&O coverage protects agents like John against the financial fallout of such simple yet impactful errors.

Why Do Agents Need E&O Insurance?

Several states require agents to carry E&O insurance as part of their licensing process to ensure real estate professionals are adequately protected. This mandatory coverage helps safeguard agents and clients from potential financial and legal repercussions. The following are states that have the insurance requirement:

- Colorado

- Idaho

- Iowa

- Kentucky

- Louisiana

- Mississippi

- Montana

- Nebraska

- New Mexico

- North Dakota

- Rhode Island

- South Dakota

- Tennessee

- Wyoming

For states that do not require agents to have real estate E&O insurance, each professional should still consider it individually. However, it’s worth noting that brokerages will typically carry E&O insurance that covers the entire team from any professional errors.

Real estate professionals need E&O insurance because it’s unpredictable when a claim might arise. Small everyday mistakes that might not seem like a big deal to an agent could have significant repercussions from the client’s perspective. So, agents should not jeopardize their careers or commission potential by missing out on this essential coverage.

Costs of E&O Insurance for Real Estate

The cost of real estate E&O insurance varies based on factors like the size of the business, the number of employees, and the coverage limits chosen. On average, individual real estate agents and brokers can expect to pay between $500 and $1,000 annually for their E&O insurance policy. Larger firms with more transactions may face higher premiums due to the increased risk.

The cost for your E&O insurance will vary based on:

- Geographic location: Metro areas with higher population densities may have higher premiums.

- Coverage limits: Higher coverage limits offer more protection but result in increased premiums.

- Deductible: Opting for a higher deductible usually lowers the insurance premium cost.

- Experience and history: Agents with more experience and a clean claims record can often secure lower premiums.

- Brokerage size and type: The cost may vary depending on the brokerage’s overall risk profile assessed by the insurance company.

- Individual risk assessment: Premium rates can also be influenced by transaction volume and the types of properties handled.

The cost of E&O insurance might seem like an additional expense, especially when working as an independent contractor. However, it is a worthwhile expense of your real estate salary, considering the potential financial impact and the fact that legal fees can add up quickly.

How to Select an E&O Insurance Provider

All real estate professionals should start by researching providers specializing in E and O insurance real estate coverage. These providers will better understand the specific risks associated with your profession. Evaluate their reputation by reading reviews and seeking recommendations from colleagues. Compare coverage options to ensure comprehensive protection for claims, including misrepresentation and failure to disclose important information.

It’s important to pay attention to the policy limits and deductibles to balance adequate coverage with affordable premiums. Additionally, assess their claims process to ensure it’s straightforward and responsive, as timely support is critical during disputes. By carefully selecting an E&O insurance provider, you can secure reliable protection and focus on growing your real estate business with confidence.

ERGO – Next Insurance is a top choice for real estate professionals seeking errors and omissions insurance in real estate. They offer a streamlined, user-friendly experience tailored for small businesses. They also provide quick quotes online, allowing you to get a customized policy within minutes without any hassle. ERGO – Next Insurance also specializes in other real estate insurances like general liability and worker’s compensation, so real estate professionals can take advantage of their bundled pricing offers.

How to File a Claim Through E&O

Filing a claim under your E&O insurance can seem daunting, but understanding the process ensures you receive the necessary support. When you think a mistake might lead to a claim, acting promptly and following the correct steps can help you avoid the situation. Here’s a breakdown of what you need to do to file a claim effectively:

- Notify your insurance provider immediately: As soon as you become aware of a potential claim, notify your insurance provider. This includes any written demand, lawsuit, or situation that might lead to a claim.

- Early notification: Promptly notifying your insurer is crucial as it allows them to investigate and respond effectively.

- Gather documentation: Collect all relevant documents related to the claim, such as contracts, communications, and other pertinent information.

- Submit documents: Provide these documents to your insurer to support your claim.

- Insurer review: Your insurance company will review the details of the claim.

- Resolution: The insurer will work with you to resolve the issue through settlement negotiations or legal defense in court.

- Maintain communication: Keep open communication with your insurer throughout the process to ensure a smoother resolution.

Bringing It All Together

Having E&O insurance is a must to protect your career and financial stability. Every real estate professional should understand common errors and know what the insurance covers to help safeguard them against the unpredictable challenges of the industry. Whether it’s mandatory or not, this insurance gives you the confidence to navigate potential legal disputes while continuing to build trust with your clients.

By staying informed and prepared, you can focus on delivering top-notch service and keeping your real estate GCI and livelihood secure. With E&O insurance in your corner, you can tackle any challenge that comes your way, knowing that you’ve got the support you need to handle unexpected bumps in the road. So go ahead and keep those transactions smooth and your clients happy.