This guide is for real estate investors and borrowers who need fast, flexible financing and want help finding the right hard money lender. Hard money loans can bridge the gap between securing funds and purchasing a property, especially if you do not qualify for a traditional bank loan. Although they are usually more expensive than conventional financing, they can be a practical option for fix-and-flip projects, time-sensitive investments, or other short-term real estate needs.

To help you determine where to start when searching for the right hard money lender, take a look at the few I’ve reviewed below:

| Kiavi | Overall pick for favorable rates and terms | |

| RCN Capital | Investors with varying experience | |

| Lima One Capital | Various investment strategies | |

| New Silver | Instant loan approvals | |

| Easy Street Capital | Quick funding speeds |

- The Close’s top picks for the best hard money lenders

- Kiavi: Best overall for favorable rates and terms

- RCN Capital: Best for investors with varying experience

- Lima One Capital: Best for various investment strategies

- New Silver: Best for instant loan approval

- Easy Street Capital: Best for quick funding speeds

- How to choose a hard money lender

- Methodology: How I chose the best hard money lenders

- Alternatives to hard money loans

- Frequently asked questions (FAQs)

- Your take

The Close’s top picks for the best hard money lenders

QuickBooks has paid for this placement. However, our team of experts approved QuickBooks as an appropriate product and our content remains editorially independent.

Stay lender-ready. QuickBooks generates up-to-date P&Ls and cash-flow reports lenders ask for. No manual spreadsheets required. — Receive 50% off QuickBooks for your first 3 months.

Kiavi: Best overall for favorable rates and terms

Pros | Cons |

|

|

|

|

|

|

| |

Rates & terms

- Starting interest rate: 7.75%

- Loan-to-value ratio (LTV): 95% LTC (loan-to-cost), covering up to 100% of rehab costs, 80% ARV (after-repair value)

- Upfront fees: No upfront fees; 1.5% to 3% origination fee

- Term: 12, 18, and 24 months

- Credit requirement: 660

- Min and max loan amount: $100,000 to $3 million

- Prepayment penalty: Yes

- Property types: Single-family homes, attached and detached planned unit developments (PUDs), and 2-4 unit rentals

Why I chose Kiavi

For fix-and-flip investors, Kiavi stands out as a strong financing option. It offers fix-and-flip financing with a streamlined underwriting process designed to help you secure funding quickly. In some cases, you can close in as little as seven days, which can improve your ability to compete with cash buyers and start renovations even sooner.

Kiavi also aims to keep the early stages straightforward, with no application fees or income verification required to get started. With competitive starting rates and flexible eligibility criteria, it can be a practical choice for both experienced investors and newer flippers who may not yet have an extensive track record.

Additional features

- Prequalification: With just a soft credit pull, real estate investors can prepare to make quick offers on any opportunities that arise.

- Flexible loan amounts: With loans up to $3 million, Kiavi can accommodate a wide variety of project needs, from small renovations to large-scale projects.

RCN Capital: Best for investors with varying experience

Pros | Cons |

|

|

|

|

|

|

|

|

Rates & terms

- Interest rate: 9.24%

- Loan-to-value ratio: Up to 95% of the purchase price, 100% of renovation cost (not to exceed 75% of ARV)

- Term: 12 to 18 months

- Upfront fees: No upfront fees. 3% to 6% origination fee

- Credit requirement: 650

- Min and max loan amount: $75,000 to $3 million

- Prepayment penalty: No

- Property types: Non-owner occupied 1-4 family real estate, condos, townhomes, 5+ unit apartments, and mixed-use properties

Why I chose RCN Capital

RCN Capital works well for investors at a range of experience levels because it offers multiple loan options to match different project types. With relatively high lending limits, it can support everything, from larger development deals to financing multiple rental properties. Loan amounts are based on the specific program and the value of the property used as collateral, and your experience can influence the available rate and LTV. Even so, its rates, terms, and qualification standards remain competitive.

Another advantage is that you pay interest only on the funds you’ve drawn, not on renovation funds that are still held back. And because there are no prepayment penalties, you can pay the loan off early and potentially reduce your total borrowing costs. The application process is straightforward and can be completed online, typically requiring a credit review, background check, bank statements, and a property appraisal.

Additional features

- Rehab Budget Builder: This tool is available to help investors analyze their investments to understand cost, risk, ROI, etc.

- Video library: It includes up-to-date videos that offer market updates, investment tips, and motivational content.

Lima One Capital: Best for various investment strategies

|

|

|---|---|

Pros | Cons |

|

|

|

|

|

|

Rates & terms

- Interest rate: Varies

- Loan-to-value ratio: 92.5% of LTC, 75% ARV

- Term: 13, 19, and 24 months

- Upfront fees: Varies

- Credit requirement: 600

- Maximum loan amount: Varies

- Prepayment penalty: None

- Property types: Townhouse, single-family, multiunit up to 4; not for owner-occupied properties

Why I chose Lima One Capital

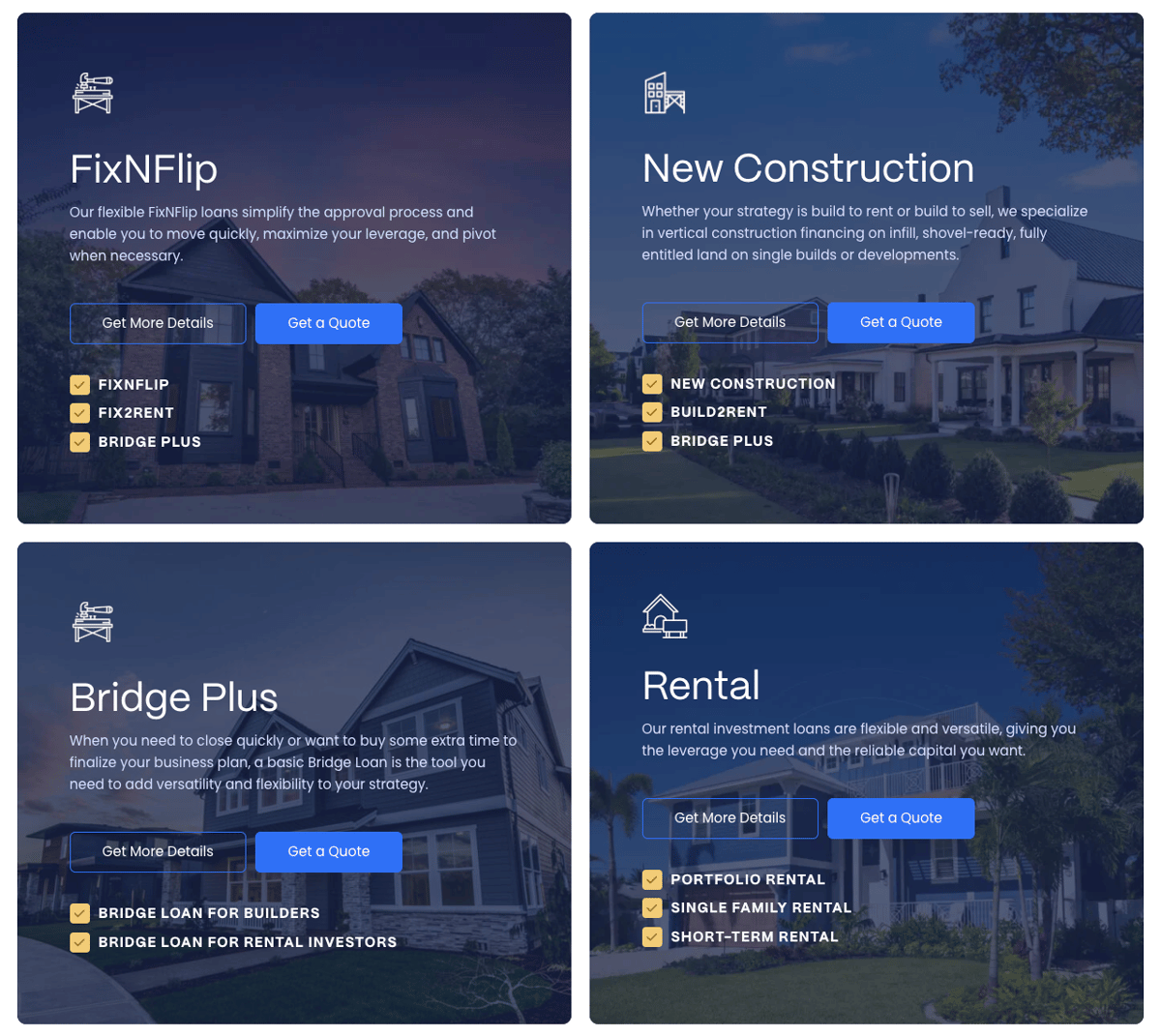

Lima One Capital offers a broad mix of financing options that can support several real estate investment strategies, like rental properties, new construction, multifamily projects, and short-term rentals. It also provides a range of loan structures and terms, making it easier to align financing with the specifics of your deal. With repayment terms of up to 24 months, it can be a solid fit for experienced investors who want the flexibility to execute and exit projects on an accelerated timeline.

Its eligibility requirements tend to be relatively flexible, though your exact rate, terms, and conditions will depend on factors like credit profile, investing experience, and the goals of the project.

Additional features

- Case studies: Detailed case studies on the website illustrate the strategies, financial figures, challenges, and outcomes of real-world property investments.

- Podcast: A podcast covers various topics relevant to real estate investing and provides ongoing education and industry insights in an easily accessible audio format.

New Silver: Best for instant loan approval

Pros | Cons |

|

|

|

|

|

|

Rates & Terms

- Interest rate: 9% to 11%

- Loan-to-value ratio: 90% of LTC, 75% ARV

- Term: 18 months

- Upfront fees: 1% to 1.75% origination fee, $1,000 underwriting fee, $1,350 legal fee

- Credit requirement: 650

- Maximum loan amount: $100,000 to $5 million

- Prepayment penalty: None

- Property types: Residential 1 to 4 units, condos, townhomes

Why I chose New Silver

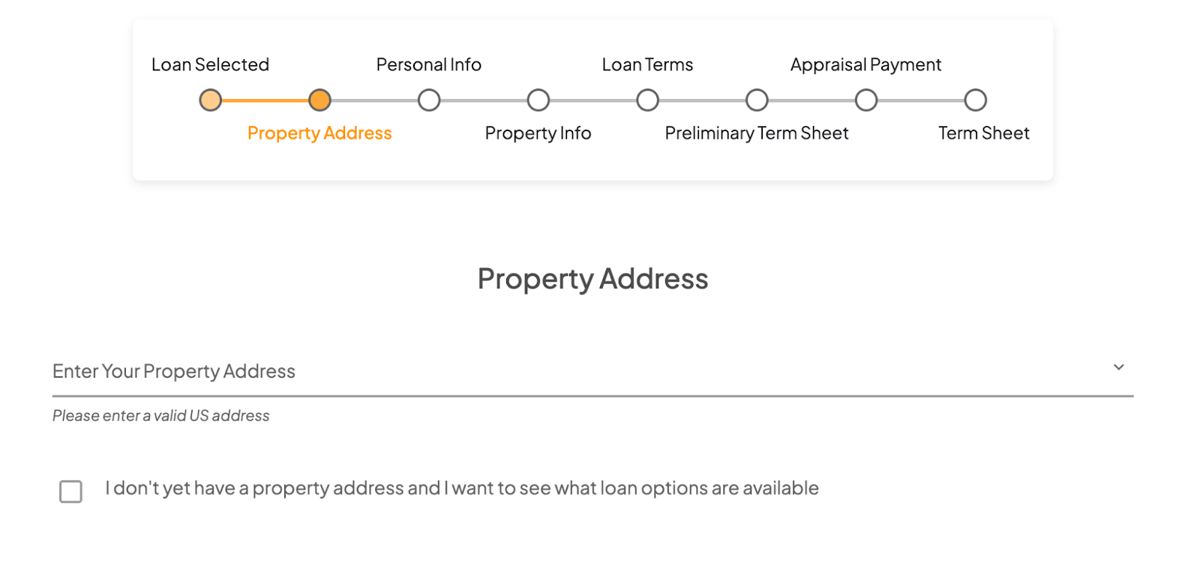

New Silver stands out for its fast, tech-forward lending process, designed to move fix-and-flip deals along quickly. Its AI-driven platform supports near-instant online decisions, and the application can take as little as five minutes to complete. Closings can also happen on an accelerated timeline, in some cases in as few as five days.

Because the loan is secured by the property, the upfront requirements are relatively light. You can typically get started with a soft credit check and a property value review without income verification. This reduces paperwork and shortens the time between application and funding availability for your project.

Additional features

- Advantage Program: Enhanced loan terms and rates for repeat borrowers who have successfully completed previous projects with New Silver.

- The Lender Blog: An up-to-date blog covering various real estate topics such as strategy, market trends, and success stories.

Easy Street Capital: Best for quick funding speeds

Pros | Cons |

|

|

|

|

|

|

Rates & terms

- Interest rate: Starting at 8.90%

- Loan-to-value ratio: Up to 93% LTC (90% of Purchase, 100% of Rehab)

- Term: 6 to 18 months (with extension options)

- Upfront fees: $1,995 Doc fee

- Credit requirement: 600

- Maximum loan amount: $75,000 to $5 million+

- Prepayment penalty: None

- Property types: Residential (SFR & 2-4 Unit)

Why I chose Easy Street Capital

Easy Street Capital offers financing for fix-and-flip, rental, and construction projects, but its EasyFix program is especially appealing for investors who value speed. With competitive starting rates and a notably fast approval and funding process, it can be a smart option if you need to close quickly or strengthen your position against competing offers.

It’s also a relatively accessible lender, thanks to a low minimum credit score requirement. Loans are available across much of the US (state availability varies), and financing is available for residential properties with two to 10 units. Additional cost-saving perks include no appraisal requirement and no prepayment penalties. The application process is straightforward and light on documentation, and many borrowers receive a term sheet within 24 hours. You can apply online or connect with a representative to get started.

Additional features

- Available investment properties: Listings provided on the website showcase potential real estate investment opportunities to take advantage of.

- Industry insights: Articles that reference industry terms, trends, and insights for interested investors.

How to choose a hard money lender

Whether you’re a seasoned investor or a first-timer, working with the right hard loan lenders is vital to the success of your project. It’s important to carefully consider your options and determine your budget and strategy. With a background in commercial real estate, I think it’s best to keep these factors in mind when on the lookout for the top hard money loan lenders:

- Lender reputation: Research the lender’s track record, customer reviews, and industry reputation to ensure they are reliable and fair.

- Loan terms: Fully comprehend all loan terms, including interest rates, fees, loan-to-value ratio, and repayment schedule.

- Speed of funding: Since time is often critical, assess how quickly the lender can process and fund the loan.

- Professional advice: Consider consulting with a financial advisor or real estate professional to help navigate the process and select the best lender for your unique needs.

- Compare multiple offers: Don’t settle for the first lender you meet. Compare different offers to find the best terms and rates.

- Transparency: Ensure the lender is transparent about all costs, fees, and any penalties associated with the loans.

Methodology: How I chose the best hard money lenders

We use a methodology focused on the most critical factors to identify the top hard-money lenders for real estate and produce an unbiased review. I reviewed various lenders against multiple key factors to ensure I viewed them through the lens of what would be most important to a potential real estate investor. The detailed analysis then identified lenders that offer solid financial solutions and align well with various investment strategies and goals.

Key factors involved with this process included the following:

- Interest rates and loan terms: Compared pricing and term options across lenders to see which ones offered the strongest combination of affordability and flexibility.

- Speed of loan processing and funding: Reviewed how quickly each lender typically moves from application to approval with the financing, since timing can be the difference in competitive deals.

- Lender reputation: Looked at borrower feedback and broader industry sentiment to evaluate reliability, consistency, and overall customer experience.

- Transparency: Assessed how clearly each lender explains fees, conditions, and requirements upfront to help avoid surprises at closing.

- Geographical coverage: Considered the availability of services across different regions to accommodate investors in various locations.

- Target audience suitability: Analyzed which types of real estate investors (e.g., fix-and-flippers, buy-and-hold investors, and commercial developers) best cater to them based on their product offerings and specialty areas

Alternatives to hard money loans

If you think a hard money loan might be too risky, there are some alternatives you can consider instead. This could include:

- Commercial real estate (CRE) loans: It may be worth considering a traditional CRE loan rather than a hard-money loan. Whether you’re looking to purchase, renovate, or refinance, CRE loans have flexibility. These loans typically offer more favorable rates and carry less risk than hard-money loans. For some options, check our roundup of the best CRE loans.

- Business line of credit: A business line of credit can provide you with access to funds on an as-needed basis. If you need flexibility to purchase a property on the fly, a business line of credit can help you do it. You only pay interest on what you borrow, and you’ll have the ability to repay over time.

- Home equity line of credit (HELOC): A home equity line of credit can be used to finance the acquisition of a property, and its limit is tied to the value of your home. Similar to a business line of credit, you can use it as needed and repay the balance over time.

Frequently asked questions (FAQs)

Hard money loans usually cost more than traditional bank financing. Because these loans are designed for speed and are backed primarily by the property, lenders often offset the added risk with higher interest rates and upfront fees. Pricing can vary significantly depending on factors like your credit profile, the property itself, the deal structure, and the lender’s criteria, but most borrowers typically see rates in the 7% to 15% range, sometimes higher.

One of the biggest advantages of a hard money loan is how quickly you can get funded. Depending on the lender and deal, you may be able to move from application to closing in just a few days; seven to 10 days is typical. That speed can be especially helpful if you’re up against cash offers or working with a tight project schedule.

Hard money loan terms can differ significantly based on the lender and the specifics of the deal. That said, most follow a similar structure, with short repayment timelines, interest-only payments during the loan term, and a larger balloon payment due at the end. The property itself typically serves as the primary collateral.

Your take

Hard money loans can be a powerful tool when you need speed, flexibility, or asset-based financing to secure a time-sensitive deal. At the same time, the higher rates, fees, and shorter repayment timelines mean they’re best used with a clear plan for renovations, holding costs, and your exit strategy.

I recommend using this guide as a starting point, then comparing a few lenders side by side. The right choice should align with your timeline and property type, provide transparent terms, and offer the support you need to execute the project confidently, without unexpected costs or delays.